Why isn’t gold rising on war news?

I’ve watched gold markets for decades, and the recent move during the Iran conflict stands out as one of the most counterintuitive in recent memory.

Gold has declined roughly 3–4% since tensions escalated. Leading gold stocks have fallen even more, down 7–8% in some cases. After a powerful multi-year rally—nearly 180% from the 2022 lows—markets now appear to be pausing before the next move.

You’re reading The Growth Thesis — a publication for people who think beyond headlines.

Founded by Markus Drop, it’s built to cut through noise and focus on what actually drives long-term wealth: economic cycles, capital allocation, and investor behavior.

No hype. No speculation.

Just clear thinking for sustainable growth.

Gold Pulls Back Amid War Escalation — Defying Safe-Haven Logic

Gold has pulled back modestly since the escalation began, even as geopolitical risks intensified. The Middle East conflict has disrupted key energy routes, yet gold has not responded in the way many investors would expect from a traditional safe-haven asset.

At the same time, gold equities have experienced sharper declines, reflecting a combination of profit-taking and shifting capital flows. For portfolios heavily allocated to physical gold, this type of volatility can feel counterintuitive—but it is not without precedent.

Since the outbreak of war, gold is down roughly 3.5% – and prices of the best gold stocks are down even more. Why isn’t gold going up?

Let me explain:

First of all, gold rose roughly 180% from its bottom in 2022. A move that massive is not normal. Every repricing event is always followed by a rest.

Some of gold’s sideways price action is nothing more than gold taking a breather after a blistering run in 2024-2025.

Secondly, most people think gold is a crisis hedge that benefits when the world erupts in chaos. This is true – but probably not the way you think…

Yes, you want to own plenty of gold when the world is in chaos – like now.

But the gold price normally doesn’t go vertical when the bombs start falling.

Gold is primarily a slow-moving, long-term play on the decreasing value of paper assets and fiat currencies – aka inflation.

War will certainly accelerate the decline of the dollar’s purchasing power, but this doesn’t show up in the gold price immediately after a war begins.

In fact, the initial reaction to the war in Iran was for the dollar to strengthen.

It’s still seen as a safe-haven asset by most of the world.

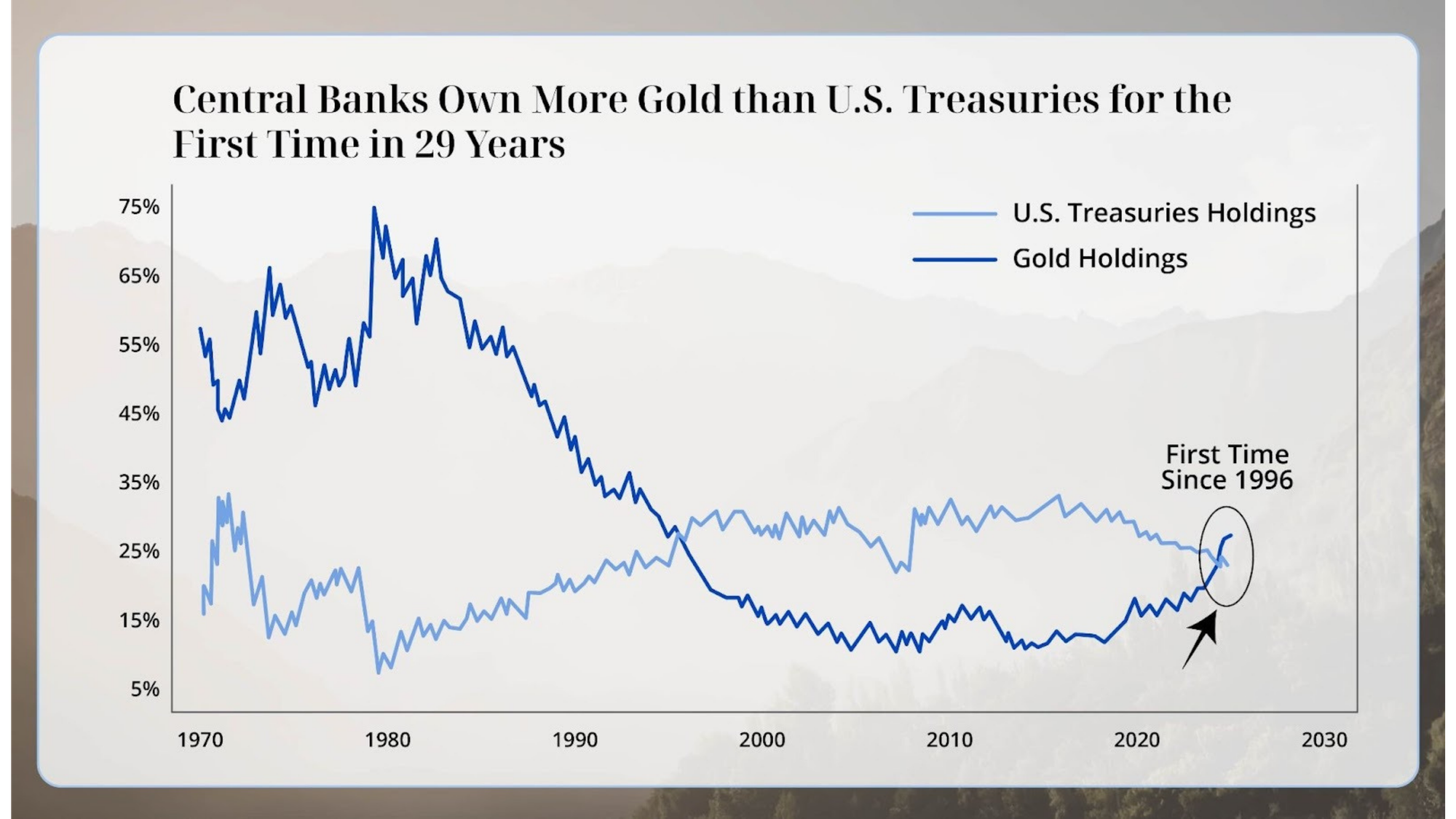

Gold is way under-owned by the average retail investor – even though central banks now hold more gold than US Treasuries for the first time in 30 years.

A big move is yet to come when retail investors finally show up. Not only that…

The dollar will eventually devalue much, much lower. It has to. All the problems that existed before the war are still present – and accelerating.

The direction of travel is still the same: The dollar is losing both value and dominance throughout the world – a trend that will continue for years to come.

As the dollar falls in value and purchasing power, it will make the gold price appear to rise.

Gold is the ultimate hedge against inflation and the policies now running the world.

That’s why you need gold. But I do not recommend buying bullion at today’s prices.

Because the best gold miners are now selling at fire-sale prices thanks to recent volatility from the war in Iran.

Conventional Wisdom: War Should Push Gold Higher

The assumption is straightforward: geopolitical conflict should drive demand for safe-haven assets.

Historically, gold has performed well during periods of market stress, often rising during major equity drawdowns. However, the relationship is not as immediate or consistent as many expect.

Recent market behavior reflects this nuance. While equities have weakened and volatility has increased, gold has not responded with a sharp upward move. Instead, other forces have taken precedence.

Why the Reaction Is Different This Time

The current environment is shaped more by macro conditions than by headlines alone.

The Federal Reserve continues to maintain relatively elevated interest rates. Higher yields increase the opportunity cost of holding gold, which does not generate income.

At the same time, the U.S. dollar has strengthened, drawing capital away from alternative stores of value. According to coverage from Reuters, early-stage crisis flows have favored dollar liquidity over traditional hedges.

Positioning also plays a role.

After an extended rally, gold entered this period with elevated expectations. Periods of consolidation following strong gains are not unusual, as investors take profits and reassess valuations.

Energy, Inflation, and Policy Uncertainty

The conflict has also pushed oil prices higher, reintroducing inflation concerns into the market.

Higher energy costs tend to feed through the broader economy, affecting production, transport, and consumer prices. Institutions such as the International Monetary Fund have noted that sustained energy shocks can lead to a combination of slower growth and persistent inflation.

This creates a complex environment.

Gold typically benefits from inflation over time—but in the short term, rising yields and policy uncertainty can offset that effect.

Long-Term Strength Remains Intact

Despite short-term weakness, the structural case for gold has not changed.

Central banks continue to accumulate gold as part of reserve diversification strategies. At the same time, global debt levels remain elevated, and long-term currency pressures persist.

These factors support gold’s role as a hedge against monetary instability.

Short-term price movements may appear disconnected from geopolitical events, but over longer horizons, gold tends to reflect underlying macro conditions more accurately.

Better Positioned Opportunities Within the Sector

What stands out in the current environment is the divergence within the gold market itself.

Gold miners have declined more than the metal, despite operating in a fundamentally supportive pricing environment. This type of dislocation often occurs during periods of uncertainty, when sentiment temporarily outweighs fundamentals.

For investors focused on long-term positioning, this creates a different type of setup—one driven less by immediate price movement and more by relative value.

Positioning for What Comes Next

The key question is not why gold isn’t rising today.

It’s whether the conditions that support gold are strengthening or weakening.

At the moment, many of those conditions—currency pressure, inflation risk, and structural imbalances—are still in place.

Markets are reacting to the first-order effects of the conflict.

But the more important shifts are happening beneath the surface, in capital flows, policy responses, and macro dynamics.