It’s Official: Gold Is Reclaiming Its Role in the Global System

Central banks are making a quiet but important shift—and most investors are only starting to notice.

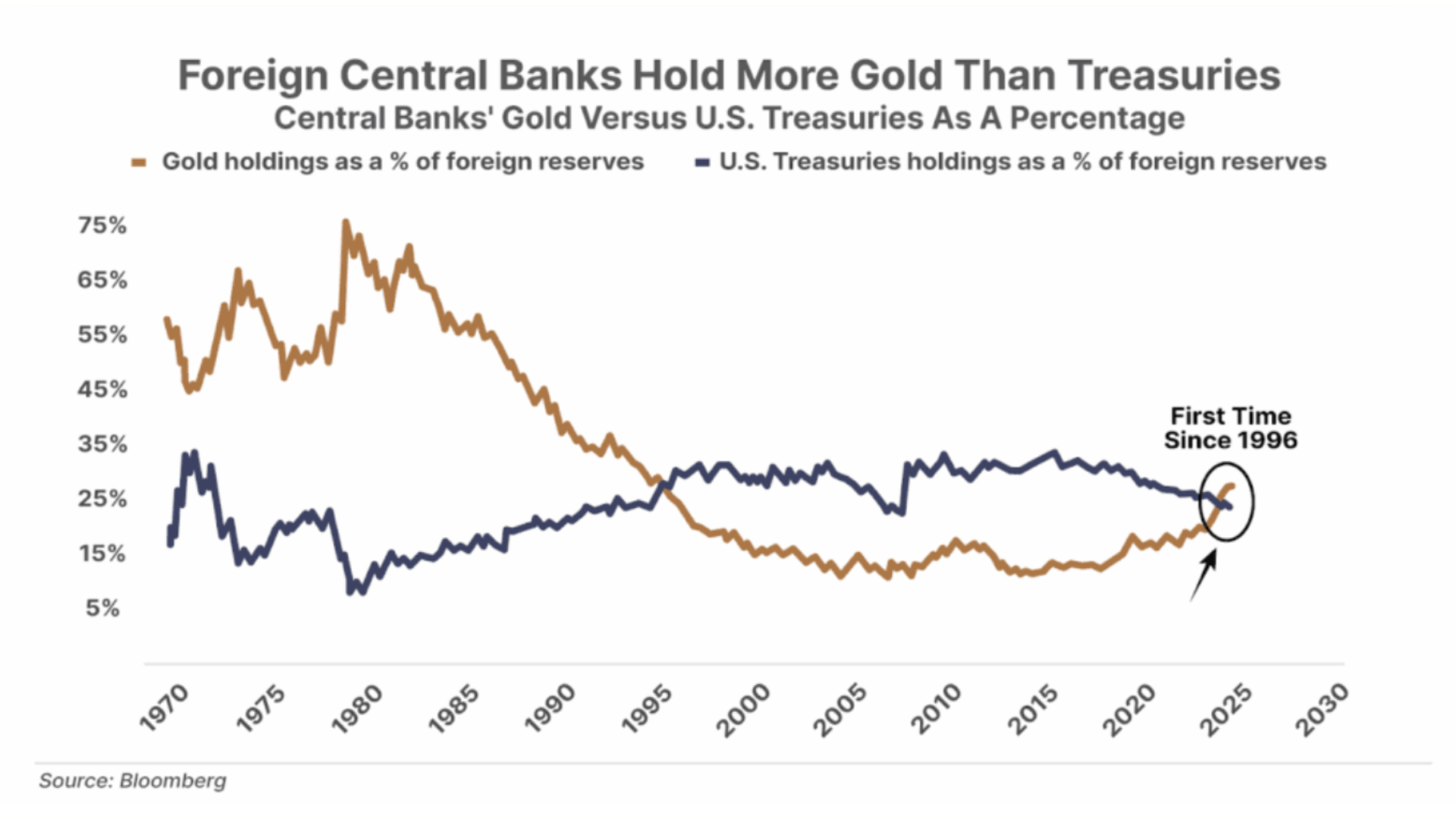

Word came recently that Central Banks now own more gold than US Treasuries for the first time in 30 years. But that’s not the big news…

The real story is the chart below…

The world has become so accustomed to holding US paper, most investors today can’t imagine anything else.

But as recently as 1980, Central Banks held as much as 70% of their reserves in gold. To return to that level, gold demand would have to increase 3X or more.

And that’s exactly what I’m expecting.

Remember, Central Banks are price-insensitive. Unlike you and me, they simply don’t care what the gold price is. They buy because their mandate is stability.

It pains me to say this, but I wouldn’t be doing my job if I didn’t…

US Treasuries – the backbone of the world’s financial system for nearly 40 years – are no longer risk-free.

The world is moving away from US paper – and into gold.

What that means for you is that a small stake in the best gold companies…

Could net you an absolute fortune over the next decade.

The Shift Isn’t Sudden—It’s Structural

The idea that gold is “replacing” U.S. Treasuries can sound dramatic. In reality, what we’re seeing is more nuanced—and more important.

Central banks are not abandoning Treasuries. They are diversifying.

Since 2022, global central bank gold purchases have accelerated to the highest levels in decades. Countries like China, India, and several emerging markets have been steadily increasing their gold reserves while reducing reliance on dollar-denominated assets.

This isn’t a short-term trade. It’s a long-term rebalancing.

And it reflects a deeper change in how countries think about risk.

Why Gold Is Back in Focus

For most of the past 30–40 years, U.S. Treasuries served as the ultimate reserve asset. They offered liquidity, stability, and yield—all supported by the credibility of the U.S. financial system.

That foundation hasn’t disappeared. But it has become more complicated.

U.S. debt levels have climbed to record highs, and interest costs are rising alongside them. At the same time, inflation—while lower than its 2022 peak—remains structurally above the levels that defined the pre-2020 era.

For central banks, this creates a dilemma.

Holding reserves in a single currency exposes them to policy decisions they don’t control. Holding gold, by contrast, removes that dependency.

Gold doesn’t generate yield. But it doesn’t rely on anyone else’s balance sheet either.

That distinction matters more in a world of rising debt and shifting geopolitics.

The Return of “Neutral” Assets

One way to understand gold’s resurgence is to think of it as a neutral asset.

Treasuries are tied to the U.S. economy and its fiscal policy. Gold is not.

In periods of stability, that distinction doesn’t matter much. But in periods of uncertainty—whether economic, political, or geopolitical—it becomes far more relevant.

This is one reason why central banks continue to accumulate gold even as prices move higher. Their objective isn’t short-term return. It’s long-term resilience.

And that behavior tends to reinforce trends rather than reverse them.

For individual investors, the takeaway isn’t that Treasuries are obsolete or that gold replaces a diversified portfolio.

It’s that the balance is changing.

The traditional model—where bonds provide safety and equities provide growth—is being tested in an environment where both inflation and debt levels are elevated.

That doesn’t break the system. But it does require adaptation.

Gold, along with other real assets, is increasingly being viewed as a complement rather than an alternative. It plays a different role—one tied less to income and more to protection against systemic risk.

Why This Cycle May Look Different

Gold has gone through multiple cycles over the past few decades. What makes the current one different is the combination of forces behind it.

This isn’t just about inflation. It’s about currency diversification, geopolitical fragmentation, and long-term fiscal trends converging at the same time.

Central banks are not reacting to a single event. They are adjusting to a changing global landscape.

And because they operate on multi-decade horizons, their actions tend to be persistent.

That’s what makes this shift worth paying attention to.

It’s easy to focus on price—whether gold is up or down in a given month.

But the more important story is positioning.

When the largest and most patient players in the system begin to rebalance, it often signals a deeper transition already underway.

Gold isn’t replacing the financial system. But it is reclaiming a larger role within it.

And for long-term investors, understanding that shift may be more valuable than trying to time it.